The Buzz on Mortgage Investment Corporation

The Buzz on Mortgage Investment Corporation

Blog Article

Little Known Questions About Mortgage Investment Corporation.

Table of Contents10 Simple Techniques For Mortgage Investment CorporationMortgage Investment Corporation for BeginnersThe 8-Minute Rule for Mortgage Investment CorporationThe 10-Minute Rule for Mortgage Investment CorporationThe Definitive Guide to Mortgage Investment CorporationMore About Mortgage Investment Corporation

After the loan provider markets the car loan to a home loan financier, the lender can use the funds it obtains to make more financings. Supplying the funds for lending institutions to create even more lendings, financiers are crucial because they establish guidelines that play a duty in what kinds of lendings you can get.As house owners repay their home loans, the repayments are gathered and dispersed to the personal capitalists that purchased the mortgage-backed securities. Unlike government agencies, Fannie Mae and Freddie Mac don't insure fundings. This implies the exclusive investors aren't guaranteed payment if consumers do not make their loan settlements. Since the capitalists aren't secured, adapting car loans have more stringent standards for figuring out whether a customer certifies or not.

Department of Veterans Affairs establishes standards for VA finances. The United State Division of Farming (USDA) establishes standards for USDA lendings. The Government National Mortgage Organization, or Ginnie Mae, looks after federal government home funding programs and guarantees government-backed financings, protecting exclusive capitalists in situation consumers default on their loans. Jumbo lendings are mortgages that surpass adapting financing limitations. Due to the fact that there is more danger with a bigger home loan quantity, jumbo car loans have a tendency to have more stringent debtor eligibility requirements. Financiers additionally manage them differently. Standard big finances are typically as well big to be backed by Fannie Mae or Freddie Mac. Instead, they're sold directly from lenders to exclusive capitalists, without entailing a government-sponsored venture.

What Does Mortgage Investment Corporation Mean?

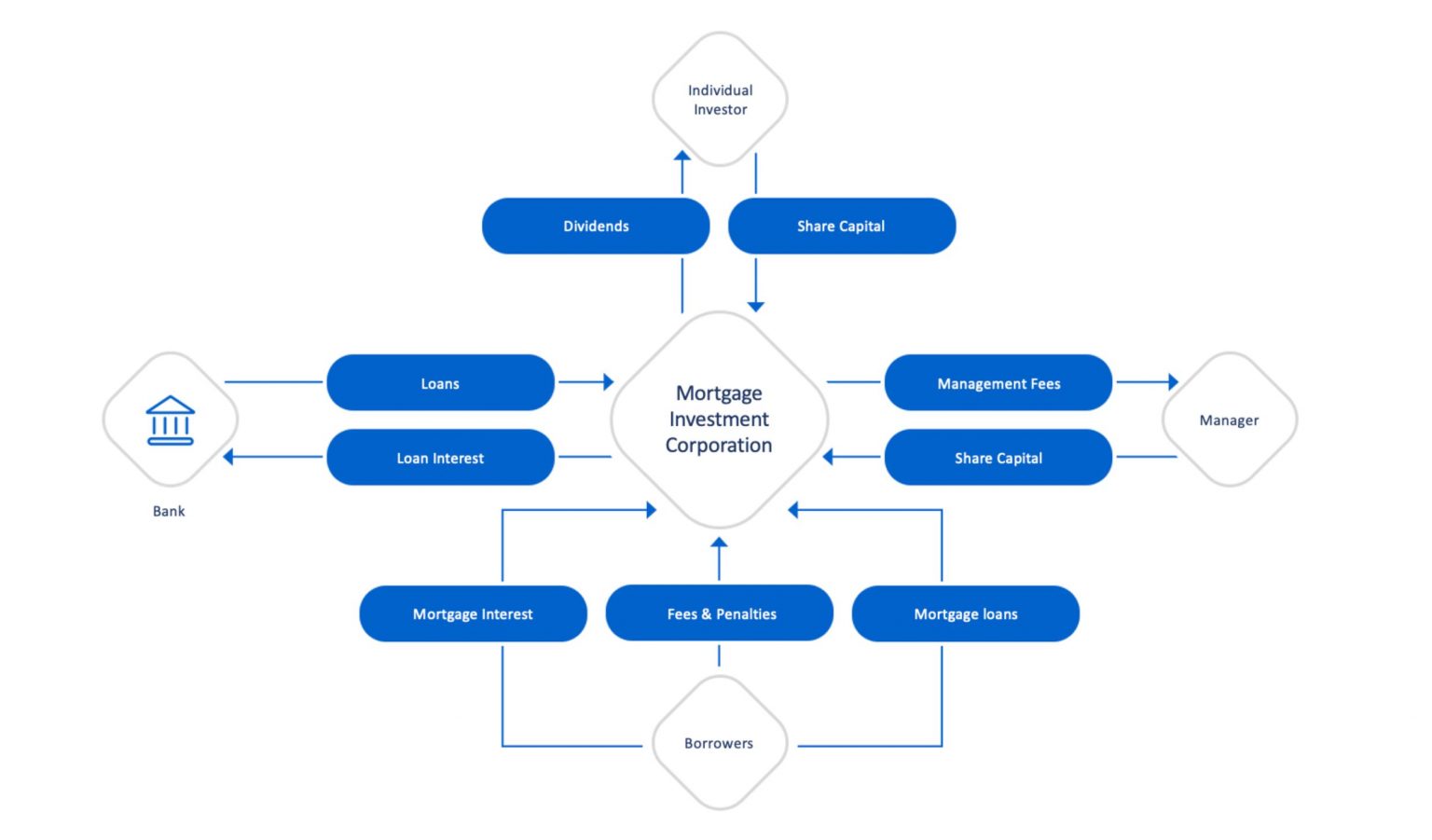

How MICs Source and Adjudicate Loans and What Takes place When There Is a Default Home loan Financial investment Companies offer capitalists with direct exposure to the property market with a pool of meticulously selected home mortgages. A MIC is in charge of all aspects of the home mortgage investing procedure, from source to adjudication, including everyday administration.

CMI MIC Finances' extensive certification procedure enables us to manage home mortgage quality at the really beginning of the financial investment process, reducing the potential for repayment issues within the loan portfolio over the term of each home mortgage. Still, returned and late settlements can not be proactively managed 100 per cent of the moment.

Some Of Mortgage Investment Corporation

We purchase home mortgage markets across the country, enabling us to lend throughout Canada. To get more information regarding our investment procedure, call us today. Contact us by completing the type listed below for additional information regarding our MIC funds.

A MIC is also thought about a flow-through financial investment car, which implies it needs to pass 100% of its yearly net income to the shareholders. The dividends are paid to capitalists on a regular basis, typically every month or quarter. Mortgage Investment Corporation. The Earnings Tax Obligation Act (Section 130.1) details the requirements that a firm need to meet to certify as a MIC: At least 20 shareholdersA minimum of 50% of properties are property home mortgages and/or money down payments insured by the Canada Down Payment Insurance Firm (CDIC)Much Less than 25% of resources for every shareholderMaximum 25% of resources spent right into real estateCannot be included in constructionDistributions submitted under T5 tax formsOnly Canadian home loans are eligible100% of take-home pay mosts likely to shareholdersAnnual monetary statements audited by an independent bookkeeping firm The Home loan Investment Firm (MIC) is a specific economic entity that invests largely in mortgage

At Amur Resources, we intend to supply a really diversified method to different investments that make best use of return and capital preservation. By providing a variety of conventional, income, and high-yield funds, we accommodate a variety of investing objectives and preferences that fit the requirements of every specific financier. By purchasing and holding shares in the MIC, shareholders get a proportional possession rate of interest in the firm and obtain income via dividend payouts.

Furthermore, 100% of the financier's funding gets put in the selected MIC without upfront transaction costs or trailer fees. Amur Resources is concentrated on giving financiers at any type of level with accessibility to skillfully managed personal mutual fund. Investment in our fund offerings is readily available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan locals and should be made on a private positioning basis.

The Buzz on Mortgage Investment Corporation

Spending in MICs is a wonderful way to get exposure to Canada's successful property market without the demands of active residential or commercial property administration. Other than this, there are a number of other reasons why financiers consider MICs in Canada: For those looking for returns equivalent to the stock market without the associated volatility, MICs supply a safeguarded property financial investment that's less complex and might be a lot more profitable.

As a visit our website matter of fact, our MIC funds have historically provided 6%-14% yearly returns. * MIC capitalists receive returns from the passion payments made by consumers to the mortgage loan provider, forming a constant easy revenue stream at greater rates than traditional fixed-income protections like government bonds and GICs. They can likewise pick to reinvest the returns right into the fund for worsened returns.

MICs presently make up roughly 1% of the general Canadian mortgage market and represent a growing section index of non-bank financial companies. As financier demand for MICs expands, it is necessary to understand exactly how they work and what makes them different from typical realty investments. MICs buy home mortgages, unreal estate, and for that reason offer direct exposure to the housing market without the included risk of building ownership or title transfer.

Some Known Questions About Mortgage Investment Corporation.

typically in between six and 24 months). In return, the MIC gathers rate of interest and fees from the borrowers, which are then dispersed to the fund's preferred investors as dividend settlements, normally on a month-to-month basis. Because MICs are not bound by many of the very same rigorous lending requirements as conventional banks, they can set their own standards for accepting fundings.

Situation in point: The S&P 500's REIT group significantly underperformed the more comprehensive securities market over the past 5 years. The iShares U.S. Property exchange-traded fund is up less than 7% since 2018. By contrast, CMI MIC Funds have historically created anywhere from 6% to 11% yearly returns, depending on the fund.

In the years where bond yields constantly decreased, Home mortgage Financial investment Companies and other different assets expanded in appeal. Returns have rebounded given that 2021 as main financial institutions have raised rates of interest but genuine yields stay adverse about inflation - Mortgage Investment Corporation. Comparative, the CMI MIC Balanced Home loan Fund created a net yearly return of 8.57% in 2022, not unlike its efficiency in 2021 (8.39%) and 2020 (8.43%)

The Best Strategy To Use For Mortgage Investment Corporation

MICs give capitalists with a way to spend in the real estate market without in fact possessing physical residential or commercial property. Instead, capitalists pool their cash with each other, and the MIC makes use of that cash to fund home mortgages for borrowers.

Report this page